The words ‘capital’ and ‘preservation’ are some of the most reassuring in the English language, particularly at a troubled economic and political moment in history.

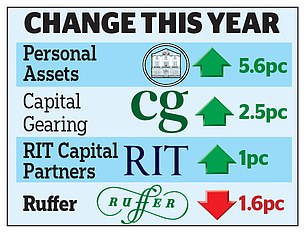

This is why investors are looking again at the capital preservation trusts – Capital Gearing, Personal Assets, RIT Capital Partners and Ruffer. These aim to provide a buffer when stock markets turn stormy and global conflicts mount.

One of these trusts, the £2.7billion RIT Capital Partners, shelters some of the wealth of the Rothschild dynasty, illustrating that even the seriously moneyed consider diversification against adversity as worthwhile.

Some of the interest in the capital preservation sector is being spurred by the chance for bargain-hunting.

Against the background of the love affair, with shares in Amazon, Nvidia and other US tech titans, the share prices of the capital preservation trusts have declined, meaning that some stand at a discount to their net asset value (NAV). RIT Capital Partners is at a 26.85 per cent discount. But the trust is exploiting this shortfall to win a new clientele, a strategy that could revive the shares.

The manager Maggie Fanari says: ‘I think we have a very compelling growth opportunity – particularly at the discount that we’re trading at today.’

Another factor behind the focus on the capital preservation sector is this week’s cut in the prize rate on the £126billion Premium Bond fund operated by National Savings & Investments (NS&I). This reduction is a reminder that 4 per cent-plus risk-free returns may not be available indefinitely.

NS&I, which is sponsored by the Treasury, provides a 100 per cent guarantee over every penny committed to its care.

The capital protection trusts cannot make such a pledge since they are not immune to turbulence. However, they do strive to provide a sanctuary when stock markets stumble – but also the potential for appreciation through their typical mix of assets: bonds, gold, currencies, commodities and shares.

Sebastian Lyon, manager of the £1.5billion Personal Assets trust, says that his mission is to ‘protect and increase (in that order)’ shareholders’ capital.

The fund is invested in index-linked bonds, but also in bullion. The price of gold, widely regarded as a safe-ish haven, is up 27 per cent this year.

Jasmine Yeo, co-manager of the £915m Ruffer trust, says: ‘We can invest in any asset in any part of the world, whether it’s shares, bonds, derivatives, commodities or currencies.’

This trust also favours overlooked and unloved ‘ugly duckling’ assets that have not much further to fall, but could turn into swans.

Peter Spiller, manager of the £947m Capital Gearing Trust, is proud to have only had two ‘down’ years in the 40-year history of the trust. Anyone who entrusted £10,000 to the trust at its launch would now have £2.2m, or £2.6m had the dividends been reinvested.

Capital Gearing’s portfolio is divided into three parts: cash, shares, UK index-linked gilts and index-linked US government bonds or ‘Tips’ (Treasury Inflation Protected Securities).

The belief is that Tips should serve as shield if higher inflation is the consequence of President-elect Donald Trump’s tariff and other policies.

These defensive offerings could be attractive to anyone who already has a cushion of savings in deposit accounts and NS&I schemes – and who suspects that their portfolio may be overexposed to US tech stocks.

This will almost certainly be your situation if your portfolio contains mostly global equity funds and trusts, many of which have placed heavy bets on the Magnificent Seven of tech – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. American exceptionalism may be here to stay. But it could be wise to have some counterbalance just in case the Trump measures trigger second-wave inflation in the US and elsewhere.

Darius McDermott, of the FundCalibre platform, points out that the performance of capital preservation trusts over the past three years has been lacklustre. RIT Capital Partners has delivered a negative return of 24 per cent over that period, but over ten years, the return is 59.7 per cent, and 7.7 per cent over one year.

In part, this is the consequence of this trust’s stakes in unquoted companies which some regard as ‘esoteric’ which seems to be a polite way of saying ‘exciting but risky’. These holdings make up close to 33 per cent of the trust. Listed shares and bonds account for the rest.

The downward pressure on all the trusts’ shares was amplified by the cost disclosure rules for all investment trusts which made their charges seem prohibitively expensive.

Although the system has been changed, this perception is likely to linger, and McDermott suspects that it will take a sharp share price downturn to bring a flood of money into the sector. But this suggests that it could be an opportune moment to pounce.

He highlights RIT Capital Partners, which could prove to be a bargain since Fanari is shifting the portfolio more into quoted stocks.

She is also attempting to improve disclosure to investors, something that other managers of all trusts and funds might contemplate. Too much of the literature remains arcane or just plain confusing.

If you find the unquoted element of RIT Capital Partners exciting, but not exactly reassuring, Interactive Investors rates Capital Gearing as one of its best-buys. This trust is at a tiny 1.97pc discount, thanks to a flurry of share buybacks.

Personal Assets is also at a minimal – 1.29 per cent – discount. Lyon candidly describes the trust as ‘an affordable luxury’, intimating that peace of mind is worth paying for.

This is something that I would agree with – which is why I will continue to hold Ruffer in the hope that the 6.37 per cent discount will narrow.

Although I am not delighted with the trust’s performance which was particularly poor in 2023, I like the blend of bonds and precious metals including silver whose price has leapt by 30 per cent this year as the consequence of a production shortfall. The demand for silver is coming from the electronics industry but the metal is also a key component in solar panels. Ruffer also has some exposure to China, a contrarian pick since this is a hazard-filled market at present.

Backing capital preservation trusts is a bet on the managers’ renewed determination to prove that they can provide a worthwhile service in what could be a tricky era.

If you want to relax back in total reassurance, stick with cash, while bearing in mind this too has an element of jeopardy. Interest rates are not going to be trimmed as fast as was expected even a month ago. Yet, over the longer term, they will head further downwards which will leave you in a less cosy state.

DIY INVESTING PLATFORMS

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.

{kind=link}